How AI Ate the World’s Memory Chips — And Why Relief Isn’t Coming Until 2028

By Andrew

Dell started raising laptop prices by as much as 30 percent in December 2025. Lenovo, HP, Acer and Asus followed within weeks, all pointing to the same culprit: they can no longer buy enough memory chips at a price that makes sense. In February, Intel CEO Lip-Bu Tan told a room at a Cisco Systems conference that he’d spoken to two of the industry’s key players and gotten the same answer from both: “There’s no relief until 2028.”

That’s not a supply hiccup. It’s a two-year forecast, delivered by the head of one of the largest chipmakers in the world, for a problem that hasn’t even peaked yet.

Every AI Chip Eats Three PC Chips

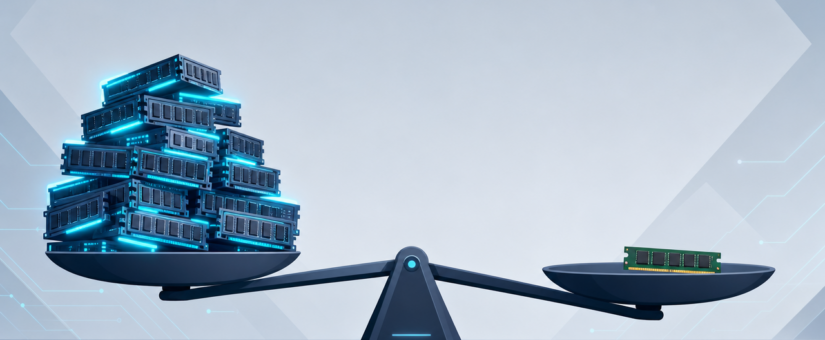

The shortage traces back to a decision made by exactly three companies. Samsung, SK Hynix and Micron control somewhere between 90 and 95 percent of the world’s DRAM production, and over the past two years they’ve been steadily shifting manufacturing capacity away from the memory that goes into your laptop and toward high-bandwidth memory, or HBM — the stacked, densely wired chips that sit next to AI accelerators in data centers.

The economics explain why. HBM commands far higher margins than commodity DDR4 or DDR5, and data centers now absorb an estimated 70 percent of all memory chips manufactured worldwide. Industry analysts put it bluntly: every AI chip produced consumes roughly the manufacturing capacity of three ordinary PC chips. In the traditional DRAM market, Samsung still leads with 38 percent share and SK Hynix holds 29 percent as of early 2026 — but in HBM specifically, SK Hynix has pulled ahead with 50 to 62 percent, with Samsung and Micron racing to catch up on the next generation, HBM4.

Building the fabs to fix this isn’t fast. Stacking memory dies with through-silicon vias — the technique HBM requires — is significantly harder to scale than standard chip production, even with unlimited capital. A new fab takes 18 to 24 months to construct, plus additional time to get manufacturing yields to a usable level. Ground broken today wouldn’t reach volume production before 2028, which is exactly the number Tan cited.

Why This Isn’t 2017 Again

The industry has been through memory shortages before, and it’s tempting to assume this one will resolve the same way. It won’t, and the difference matters.

The 2016–2018 shortage was driven by smartphone makers moving to higher-capacity memory modules, compounded by yield problems at Samsung and SK Hynix. It lasted about 18 months, prices roughly doubled, and then new capacity came online and the market normalized — because manufacturers could simply ramp up existing DRAM fabs to meet the demand spike. The 2020–2021 shortage was a different animal entirely: a pandemic-driven logistics and forecasting failure that hit automakers hardest when they’d canceled chip orders early in COVID and found themselves at the back of the line when demand snapped back.

Both of those were temporary imbalances that existing infrastructure could eventually absorb. The 2026 shortage is not. Manufacturers haven’t just fallen behind demand — they’ve permanently reallocated wafer capacity from commodity memory to HBM, and that capacity isn’t coming back to DDR4 and DDR5 production once AI demand is satisfied, because AI demand shows no sign of being satisfied. Relief here doesn’t mean “existing fabs catch up.” It means new fabs get built specifically for commodity memory, which nobody currently has strong financial incentive to do while HBM margins remain this favorable.

The Price Tag, Store by Store

For consumers, the shortage shows up as a fairly blunt set of numbers. Dell’s price increases reach as high as 30 percent. Lenovo, HP, Acer and Asus have all confirmed hikes in the 15 to 20 percent range, describing it as an industry-wide response rather than a company-specific decision — which, given that all five buy from the same three memory suppliers, is a hard claim to dispute.

Smartphones aren’t exempt either. Samsung and Apple are both expected to pass higher component costs on to buyers in upcoming flagship phones, since the same HBM-versus-DDR capacity fight applies to mobile-grade memory too, just with a smaller slice of the total market at stake.

One widely circulated industry estimate claims OpenAI alone has acquired roughly 40 percent of available wafer capacity for its own infrastructure buildout — a striking number, though it comes from a single industry analysis rather than a disclosed OpenAI figure, and should be read as a directional claim rather than a confirmed one. Even without that specific number, the broader pattern is uncontested: AI infrastructure spending is large enough to reorder a global supply chain that consumer electronics used to have mostly to itself.

A Courtroom Rerun

The reallocation to HBM has also produced a legal fight. On June 25, 2026, seventeen plaintiffs — fourteen individual consumers and three small PC-building businesses — filed a class-action lawsuit against Samsung, SK Hynix and Micron in the U.S. District Court for the Northern District of California. The complaint alleges the three companies used the shift to HBM as cover to deliberately curtail DDR3 and DDR4 production, artificially tightening the commodity market they collectively control. It cites a roughly 700 percent increase in conventional DRAM prices over four years.

Micron has denied the allegations, stating it competes “vigorously, fairly and in compliance with all applicable laws” and intends to defend itself against the claims.

It’s worth noting this isn’t the first time this exact trio has faced this exact accusation. In the mid-2000s, Samsung and SK Hynix both pleaded guilty in a U.S. Department of Justice case over DRAM price-fixing between 1999 and 2002, paying $300 million and $185 million respectively. Whether the current lawsuit finds evidence of coordination or simply parallel, individually rational business decisions remains to be seen — but the history gives the accusation more weight than it might otherwise carry.

What’s harder to dispute is the timeline everyone from Intel’s CEO to the PC vendors themselves has converged on. Even in the best case, where the lawsuit changes nothing and no new capacity comes online early, buyers are looking at roughly two more years of elevated prices before the fabs being planned today can actually ship. For an industry used to memory shortages resolving in 18 months, that’s a fundamentally different kind of wait.

- On July 3, 2026

- 0 Comment